GILES RAFFERTY, Corporate Communications and Media

The findings of 2023 Edelman Trust Barometer were revealed at Davos in January, with the Australian cut of the data made public at the start of February. The Edelman global survey highlights concern around “severe polarisation” among respondents, which the PR firm interprets as people believing their society is irrevocably divided. Australia is classified as “moderately divided” which Edelman interprets as deep societal divisions whilst at the same time thinking they might be addressable.

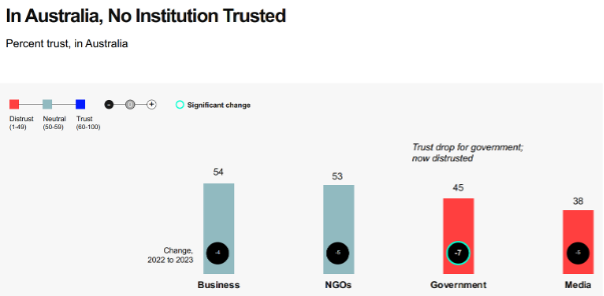

When it comes to who to trust out of Business, NGO’s, Government or The Media in addressing these perceived divisions in Australia, only Business is seen as both ethical and competent, but, disappointingly, none of these institutions are rated as trustworthy. That said Business leads the way as being neutral, neither trusted nor distrusted, alongside NGO’s while Government has sunk 7 points, compared to the 2022 survey, to join The Media as being distrusted.

On a more positive note, notwithstanding that business, as a grouping, doesn’t make it to actively trusted, according to Edelman, employers do. 75% of Australian respondents said they would trust their employer to ‘do what is right’ more than business, government, NGOs and media. The survey also reveals an expectation amongst respondents that business will take a stand on social issues and for CEOs to lead the change and be visible in doing so.

Australian CEOs expected to act on social issues

In Australia, respondents expect CEO’s to publicly take a stand on the treatment of employees (91%), climate change (78%), discrimination (75%), the wealth gap (74%) and immigration (66%). One way for CEO’s to lead change, is for them and the company they lead to be seen as a reliable source of trustworthy information. This was found to be the number one trust builder in the 2022 survey and is seen as a way for business to address societal issues without being seen as political. In addition CEO’s are expected to not only be seen to be doing good but also calling out the bad. 72% of Australian respondents expect CEOs to defend facts and expose questionable science used to justify bad social policy.

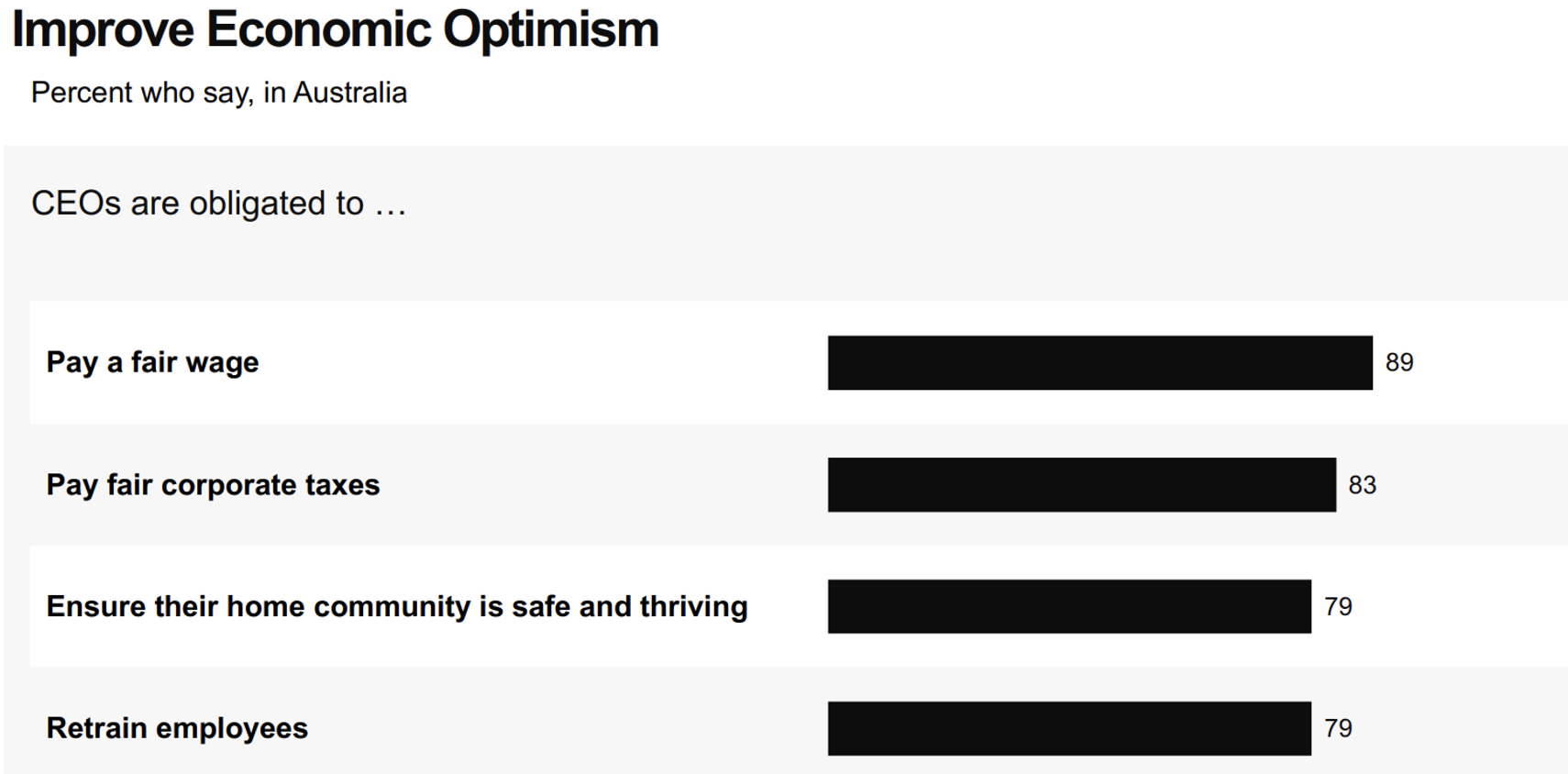

The core expectations for CEOs, as revealed by the trust survey, hit even closer to home. The majority of Australians say CEOs can help create an improved sense of economic optimism by making sure the businesses they lead invest in local communities, provide a fair level of compensation and pay a fair amount of tax. Simply stated, CEOs need to look after their own backyard and those within it.

Ironically, the Edelman Trust Barometer itself has been called into question by the media, which it claims is the least trusted. Last year the Chanticleer column in the Australia Financial Review asked two experts to assess the survey and reported it was “neither scientific nor rigorous” and anomalous with other data sets. The Guardian Australia’s coverage of the Davos launch of the global survey also claimed that Edelman was failing to take its own advice. In response Edelman point to the fact that their research and data adhered to the ESOMAR (European Society of Opinion and Marketing Research) and CASRO (Council of American Survey Research Organisations) research and ethics standards.

Trust Edelman or not, when communicating to the financial media and markets, being seen as a reliable source of trustworthy information should be non-negotiable and is central to how FIRST Advisers Media and IR teams promote our clients’ investment cases.